Approaches to Faster Settlement

Faster settlement refers to any network that settles payments, trade and transactions without that delay inherent in the daily batching and netting of transactions.

Currently, most consumer payments such as credit, debit and electronic fund transfers settle using deferred net settlement (DNS). That means funds are batched and settled at the end of a day.

As a part of the clearing process, financial institutions look at their payment balance with other banks — the amount they owe to cover payments from their account holders versus the amount owed to their account holders from other banks — and settle the net balance of those amounts with those institutions.

From an efficiency and risk standpoint, DNS is a straightforward process that allows banks to settle a large number of transactions all at once. Unfortunately for bank customers, it also introduces a significant delay in when funds move in and out of their accounts, affecting cash flow and liquidity. Additionally, it’s a system that is becoming increasingly anachronistic in a world with ever faster flowing information.

Faster settlement refers to any network that settles payments, trade and transactions without that delay inherent in the daily batching and netting of transactions. That could mean something as simple as introducing additional settlement periods during a day — meaning transactions are still batched but net positions are calculated on a more frequent basis — or actual real-time gross settlement where funds are moved directly from one account to another as soon as a transaction is approved. Regardless of the approach, the purpose is the same: reduce settlement times and reduce the friction of payments.

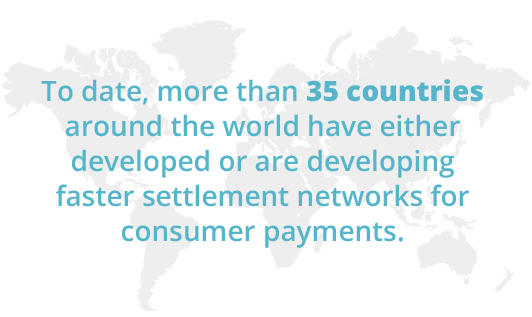

Multiple markets worldwide have begun the process of implementing networks that settle transactions more quickly or more frequently. What’s more, the number of markets announcing their plans to develop faster settlement networks is increasing as well.

The progression to real-time payment schemes provides an example of new challenges for financial institutions. The need to make decisions about accepting and settling payments immediately invalidates many of the controls currently in use. With analytics, payment platforms can mitigate the challenges these new settlement networks pose by providing the ability to respond faster.

The identification of risks such as fraud and money laundering must happen at the speed of the network. What’s more, effective analytics are constantly updating based upon past experience help the system identify future risks.

Beyond addressing the operational challenges, analytics provides new opportunities to take advantage of the data accompanying payments as well. That data set can be combined with other sources of information to perform a deeper offline inspection that detects patterns of fraud and risk that may not be obvious when payments are first analyzed during processing and settlement.